Employee’s Provident Fund (EPF) is a retirement benefit scheme for the employee which is governed by the Employees’ Provident Funds and Miscellaneous Provisions Act, 1952. It is one of the most important investment schemes for the salaried class of our country. An establishment has to compulsorily register under PF, if it employs more than 20 employees. PF is mandatory for all employees whose monthly salary is less than Rs 15,000. For such employees earning more than Rs 15,000, they can either voluntarily opt out of making contribution to the provident fund or make contribution to the provident fund only after taking permission from the employer & assistant commissioner of PF.

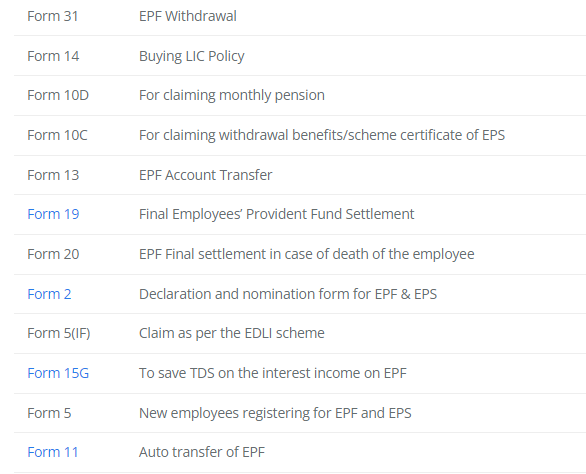

There are various forms related to Provident Fund (PF) that employees and employers may need to use for different purposes. Some commonly used PF forms include Form 19 (for final PF settlement), Form 10C (for claiming pension withdrawal), Form 31 (for partial PF withdrawal), and Form 13 (for transferring PF balance from one account to another). These forms can be obtained from the concerned PF office or downloaded from the official website.

The UAN (Universal Account Number) is a unique identification number assigned to every employee covered under the Employees’ Provident Fund scheme in India, enabling easy access and management of their PF accounts throughout their employment journey.

The due dates for Provident Fund (PF) filing can vary depending on the specific requirements and regulations of the country or region. Generally, PF contributions and related filings are required to be made on a monthly basis, with due dates falling around the 15th or 20th of the following month. However, it is essential to refer to the specific guidelines and deadlines set by the local PF authority or regulatory body for accurate and up-to-date information.

Delay in the deposit of P.F. dues attracts penal damages. Damages are levied at the following flat rates:

Delay of 0 to 2 months– @ 5 % p.a.

Delay of 2 to 4 months – @10 % p.a.

Delay of 4 to 6 months– @ 15 % p.a.

Delay more than 6 months – @ 25 % p.a. (subject to a maximum of 100%)

The EPF returns are UAN based i.e. the employer is required to first register the employees in the EPFO at employer portal for the generation of UAN or the member id wherein we will feed the details of the employees.

For the PF deduction, the maximum limit of salary of the employee is Rs 15,000 per month. This means that even if the employee’s salary is above Rs 15,000, the employer is liable to contribute only on Rs 15,000 that is Rs 1,800. The statutory compliance for PF contribution has some less known facts associated with it.

Employees contribute 12 percent of their basic pay plus DA to the EPF. Employer’s EPF contribution is equal to 12% of basic pay plus DA. The employer’s contribution of 12 percent is split into two parts: 8.33 percent goes to the employee pension plan (EPS) and 3.67 percent goes to the Provident Fund.

If we analyze the Indian Tax laws, any contribution done by the employee towards PF can be considered for Section 88 rebate. In tradition, any deduction done for PF and VPF is automatically considered for Section 88 rebate in the Income Tax module.